Trade And Finance Domain

Trade and Finance Domain Explained: A Practical Guide for Interview Preparation

Trade and finance play a critical role in enabling global commerce. From small exporters to multinational corporations, businesses rely on trade finance solutions to reduce risk, ensure timely payments, and maintain healthy cash flow. For candidates preparing for banking, trade operations, or fintech interviews, understanding this domain is a strong differentiator.

This blog breaks down the trade and finance domain in a simple, interview-friendly way.

1. What Is the Trade and Finance Domain?

The trade and finance domain covers financial instruments, processes, and systems that support domestic and international trade. It helps buyers and sellers transact safely, even when they operate in different countries with varying regulations and risks.

Core objectives include:

Reducing payment and delivery risk

Providing working capital to businesses

Ensuring trust between trading partners

Supporting regulatory and compliance requirements

2. Key Trade Finance Instruments

Interviewers often test understanding of common trade finance products.

Letter of Credit (LC)

Bank guarantees payment to the seller if conditions are met

Reduces risk for both buyer and seller

Bank Guarantee

Bank promises compensation if contractual obligations are not fulfilled

Documentary Collections

Banks handle trade documents and payments without guaranteeing funds

Trade Loans & Financing

Pre-shipment and post-shipment financing

Invoice discounting and supply chain finance

3. End-to-End Trade Finance Flow

A typical trade finance transaction includes:

Trade agreement between buyer and seller

Issuance of trade instrument (LC or guarantee)

Shipment of goods

Presentation and verification of documents

Payment, settlement, and reconciliation

Understanding this lifecycle helps candidates answer scenario-based questions effectively.

4. Key Documents in Trade Finance

Documentation is central to trade finance.

Common documents include:

Commercial invoice

Bill of lading / Airway bill

Packing list

Insurance certificate

Certificate of origin

Banks verify documents strictly, often under rules like UCP 600.

5. Risks and Compliance in Trade Finance

Trade finance involves multiple risks:

Credit risk

Country and political risk

Fraud and document discrepancies

Compliance areas include:

KYC and AML checks

Sanctions screening

Trade-based money laundering (TBML) prevention

Awareness of these risks is highly valued in interviews.

6. Technology and Digital Trade Finance

Modern trade finance is increasingly digital.

Key trends:

Electronic documents and e-Lading

Blockchain-based trade platforms

Integration with core banking and payment systems

Automation of document checking

Digital transformation is a common interview discussion topic.

7. Roles in the Trade & Finance Domain

Different roles contribute to trade finance projects:

Business Analysts define workflows, rules, and compliance needs

Product Owners prioritize trade finance features and enhancements

Operations Teams handle execution and document processing

Understanding role interactions adds practical depth to your knowledge.

Final Thoughts

The trade and finance domain combines banking expertise, international regulations, documentation, and technology. For interview success, focus on understanding instruments, end-to-end flows, risks, and compliance rather than memorizing definitions.

Strong trade finance knowledge can open doors to roles in banking, fintech, and global trade operations.

Trade & Finance Products – End-to-End Guide

Purpose of Trade & Finance

International trade involves multiple risks:

Buyer may not pay

Seller may not ship as agreed

Country, currency, and regulatory risks

Cash flow constraints

Trade finance products exist to:

Reduce payment & performance risk

Enable secure exchange of goods, documents, and money

Provide working capital financing

Support trust between unknown counterparties

End-to-End Trade Flow (Big Picture)

Commercial Contract

↓

Trade Finance Instrument Selected

↓

Goods Manufactured / Shipped

↓

Documents Created & Exchanged

↓

Payment / Financing

↓

Goods Released to Buyer

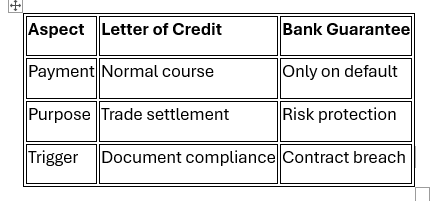

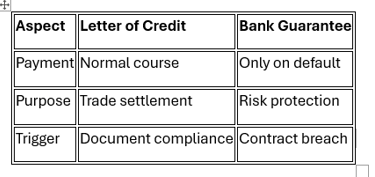

The instrument chosen (LC, BG, Collection, or Loan) determines risk level, cost, and complexity.

1. Letters of Credit (LC)

What is a Letter of Credit?

A Letter of Credit (LC) is an irrevocable commitment by a bank to pay the exporter, provided the exporter presents documents that strictly comply with LC terms.

📌 Key idea:

Banks deal in documents, not goods.

When is LC Used?

New or high-risk trading relationships

High-value transactions

Cross-border trade

Country or political risk exists

Key Parties in LC

Applicant – Importer (Buyer)

Issuing Bank – Buyer’s bank

Advising Bank – Seller’s bank

Beneficiary – Exporter (Seller)

Confirming Bank (optional)

LC End-to-End Flow (Visual)

1. Sales Contract Signed

Importer ↔ Exporter

│

2. LC Application

Importer → Issuing Bank

│

3. LC Issued

Issuing Bank → Advising Bank → Exporter

│

4. Goods Shipped

Exporter → Shipping Company

│

5. Documents Submitted

Exporter → Advising Bank

│

6. Document Check

Advising Bank → Issuing Bank

│

7. Payment

Issuing Bank → Advising Bank → Exporter

│

8. Goods Released

Importer collects goods using documents

Documents Under LC

Commercial Invoice

Bill of Lading / Airway Bill

Packing List

Certificate of Origin

Insurance Certificate

Inspection Certificate

📌 Any discrepancy = payment delay or rejection

Types of LCs (Common)

Irrevocable LC – Cannot be changed unilaterally

Confirmed LC – Additional guarantee from seller’s bank

Standby LC (SBLC) – Acts like a guarantee

Transferable LC – Used in intermediary trade

Back-to-Back LC – For traders using one LC to open another

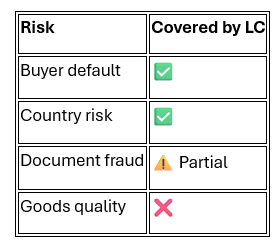

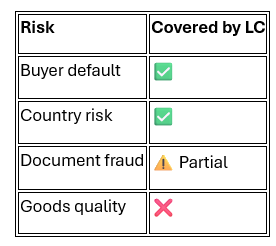

Risk Coverage

2. Bank Guarantees (BG)

What is a Bank Guarantee?

A Bank Guarantee is a bank’s promise to pay the beneficiary if the applicant fails to meet contractual obligations.

📌 Unlike LC, payment happens only if default occurs.

When is BG Used?

Construction & infrastructure projects

Tenders & bids

Long-term contracts

Advance payments

Key Parties

Applicant – Party providing guarantee

Issuing Bank

Beneficiary

Bank Guarantee Flow (Visual)

1. Contract Signed

Applicant ↔ Beneficiary

│

2. BG Issued

Applicant → Issuing Bank → Beneficiary

│

3. Contract Performance

Applicant performs obligations

│

4A. If successful → BG expires

4B. If default → Beneficiary claims BG

│

5. Bank Pays Beneficiary

Types of Bank Guarantees

Performance Guarantee

Financial Guarantee

Advance Payment Guarantee

Bid Bond

Retention Guarantee

Key Difference: LC vs BG

3. Documentary Collections

What are Documentary Collections?

Documentary Collections involve banks exchanging documents against payment or acceptance, without guaranteeing payment.

📌 Banks act as facilitators, not guarantors.

When Used?

Trusted trading relationships

Lower transaction value

Cost-sensitive trade

Types of Documentary Collections

1. Documents Against Payment (D/P)

Exporter ships goods

↓

Documents sent to Importer Bank

↓

Importer pays

↓

Documents released

2. Documents Against Acceptance (D/A)

Exporter ships goods

↓

Importer accepts time draft

↓

Documents released

↓

Payment made on maturity date

Documentary Collection Flow (Visual)

Exporter → Exporter Bank → Importer Bank → Importer

↑ ↓

Payment / Acceptance

4. Trade Loans & Trade Financing

What is Trade Financing?

Trade financing provides short-term funding to support trade before or after shipment.

📌 Focus is liquidity, not risk mitigation.

Types of Trade Loans

1. Pre-Shipment Finance

Used before goods are shipped.

Order Received

↓

Bank funds production

↓

Goods manufactured

2. Post-Shipment Finance

Used after goods are shipped.

Goods shipped

↓

Exporter receives financing

↓

Payment received later

3. Import Loans

Importer receives goods

↓

Bank pays exporter

↓

Importer repays bank later

4. Buyer’s Credit

Loan to importer (usually foreign currency)

Reduces cost for buyer

5. Supplier’s Credit

Exporter extends credit to importer

Often supported by banks

Trade Finance + Payments Integration

Trade Instrument (LC / BG / Collection)

↓

Payment Execution

(SWIFT / ISO 20022 / SEPA / RTGS)

Trade finance initiates obligation, payments move funds.

How Banks Process Trade Transactions

KYC & AML checks

Sanctions screening

Document verification

Risk assessment

Compliance (UCP 600, URDG 758, URC 522)

Accounting & settlement